Research Abstract

システミック・リスクの指標としての相互相関の変化

Changes in Cross-Correlations as an Indicator for Systemic Risk

2012年11月26日 Scientific Reports 2 : 888 doi: 10.1038/srep00888

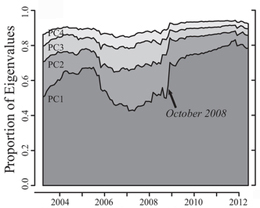

2008年から2012年にかけての世界的な金融危機は、2007年12月の世界的な景気後退に端を発し、2008年9月に悪化した。その間、米国の株式市場では、株価が2007年10月11日の高値から20%下落した。各種研究では、金融危機が株式と株価指数の相互相関およびシステミック・リスクのレベルの双方が上昇したことと関係することが報告されている。今回我々は、10種類のダウ・ジョーンズ経済部門指数を研究し、主成分分析を用いて、12か月という短期の時間枠による主成分の上昇率がシステミック・リスクの指標として実際的に利用可能であり、PC1の変化が大きいほどシステミック・リスクが増大することを示した。明らかに、システミック・リスクが高いほど、短期的に金融危機が発生する可能性は高かった。

Zeyu Zheng1, Boris Podobnik2, 3, Ling Feng4 & Baowen Li4, 5, 6

- 東京情報大学 総合情報学部 環境情報学科

- ザグレブ経済経営大学(クロアチア)

- リエカ大学 土木工学部(クロアチア)

- シンガポール国立大学大学院 総合理工学科

- シンガポール国立大学 物理学科&計算理工学センター

- 同済大学Photonicsおよび熱エネルギー研究センター&物理学およびエンジニアリング学院(中国)

The 2008–2012 global financial crisis began with the global recession in December 2007 and exacerbated in September 2008, during which the U.S. stock markets lost 20% of value from its October 11 2007 peak. Various studies reported that financial crisis are associated with increase in both cross-correlations among stocks and stock indices and the level of systemic risk. In this paper, we study 10 different Dow Jones economic sector indexes, and applying principle component analysis (PCA) we demonstrate that the rate of increase in principle components with short 12-month time windows can be effectively used as an indicator of systemic risk—the larger the change of PC1, the higher the increase of systemic risk. Clearly, the higher the level of systemic risk, the more likely a financial crisis would occur in the near future.